When the Gates Came Down: Summary of Private Credit Research in Q1/Q2 2026

A reading of 25 recent working papers on Private Credit, that's facing its first real stress test.

For a full decade, the bull case for Private Credit rested on a single reassuring claim.

That locked-up capital and patient lenders had engineered the run risk out of credit intermediation. And while deposits can flee in an afternoon, an LP commitment cannot. And the 1st Quarter 2026 tested that claim in the market.

The numbers were decidedly unsubtle. Across the 12 largest non-traded BDCs, redemption requests averaged 12.1% of net assets against a 5% quarterly cap. That’s roughly $15 billion in aggregate tender requests, which is the largest quarterly redemption pressure episode in the history of this asset class.

First Brands Group and Tricolor collapsed. JPMorgan started marking down software loans exposed to AI disruption. Apollo, Blackstone, BlackRock and some others reached for redemption gates. Securities litigation followed against Blackrock TCP Capital and Hercules Capital. Jamie Dimon (endearing chap) warned about hidden cockroaches we weren’t seeing.

It’s interesting that this all happened but its even more interesting that the system absorbed it. And in about 6 weeks, every allocator was asking if that resilience was structural or improvised.

A remarkable wave of research has landed in the last 8 months trying to answer that from various angles. So I read through 25 recent working papers (all SSRN) to get perspective. (My wife and son had opinions about my monopoly on our Brother laser printer during this period, and I had to sound apologetic about it.)

What follows is what the research objectively tells us, ordered (roughly) by how directly each bears on what just happened.

How things went down

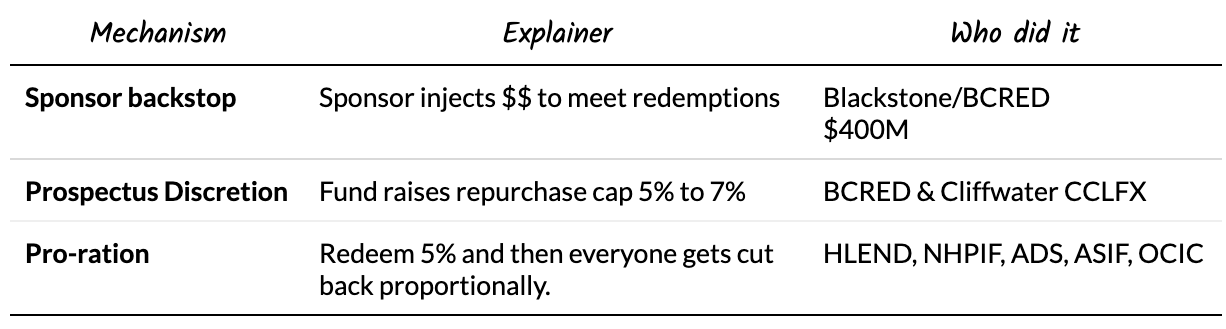

The most forensic (and sharp) account of Q1 belongs to Luka Stanisljevic [1].

- His framing is built on a structural fact that Retail Private Credit vehicles have no public lender of last resort. Ergo, the implicit value of that backstop is roughly zero.

- When the redemption wave hit, the missing backstop had to be rebuilt by hand deal by deal from private materials.

- Of all the methods available, pro-ration did the most work. The dramatic headline was the Blackstone/BCRED sponsor injection, but structurally it was the boring 5% cap/pro-rata mechanism that absorbed the broader cascade.

- The main takeaway was that Q1 2026 semi-liquid private credit redemption episode did not become catastrophic because the system had private contractual shock absorbers. More importantly those shock absorbers are fragile, unevenly disclosed, sponsor-dependent, and legally/politically sensitive.

For the balance sheet anatomy under all of this, I read the paper by Elisavet Mistopoulou and Sascha Steffen [2].

They’re basically saying that private credit fragility may sit in the funding layer above the loan book. Most private-credit commentary is around “Are the loans bad?”. Instead, this paper asks: “Even if the loans are okay, can the lender keep financing those loans?”. That’s important because in stress, the problem may not start with mass borrower defaults. It may start with banks tightening terms, refusing to renew facilities, reducing borrowing bases, or investors demanding higher yields to refinance unsecured notes.

The empirical contribution at the first facility level panel of US BDC liabilities and the scope was serious. They covered 195 BDC, over 2900+ funding facilities and $267B outstanding from ‘17-‘25.

- Fragility is the lender’s own funding stack. BDCs can still become fragile if its own debt matures, bank lines are not renewed, or collateral becomes encumbered.

- Public BDCs aren’t safer than private BDCs, they’re just fragile differently. Private BDCs are fragile through bank dependence (72% is bank originated). Public BDCs are fragile through unsecured debt maturity walls (notes coming due).

- Cash and unused lines do not reassure equity investors. Neither reduce the stock market penalty for near-term refi risk during credit stress. Investors seem to get that liquidity lines != solution to rollover risk. Makes sense, just because you have a credit card doesn’t mean your mortgage lender will refinance you.

- Emergency liquidity backstop wasn’t heavily used during redemptions. Large private BDCs didn’t sell assets or use corp credit lines. Instead they added leverage through SPV bank lines, CLO issuance and unsecured debt, growing total debt 20% on average.

- Moving from revolvers to SPV facilities onyl changed seniority and didn’t reduce bank exposure. Total banking system exposure migrated from unsecured/general claims to secured claims against pledged loan collateral. That encumbers portfolio assets that could otherwise absorb losses.

- Listing changes funding structure even within the same BDC. Listing isn’t just a cosmetic governance status, it changes the liability structure. After listing, a BDC’s unsecured debt share rises by about 17%, and reliance on bank SPV warehouse facilities falls by about 14%.

- Funding diversification is mostly about size and not public listing. Once you control for size, apparent diversification advantage of public BDC largely disappears!

- Banks discipline risky BDCs through maturity and not necessarily price. You’d expect riskier BDC to get charged higher spreads, but no, it turns out to be shorter maturities and tighter renewal exposure. That means the risk can be hidden if you only look at current interest cost. The real warning sign may be how soon does the facility mature, and who controls renewal?

Another paper by David Xiaoyu X. and Jing Huang [3] adds the off-balance-sheet piece that rarely shows up in the headline AUM number. The key question for them is how can private credit lenders promise borrowers access to future money when private credit funds themselves do not have deposits like banks?

BDCs are issuing large amount of revolving credit facilities, Delayed Draw Term Loans (DDTL) and other unfunded commitments. So much so that in 2025, commitment-to-asset ratios at BDCs were comparable to banks.

The operating media narrative was “Oh no, banks are being disintermediated!”.

Turns out:

- BDCs don’t fully back their commitments. The system only works because not everyone draws simultaneously. They compared BDC commitment books to a hypothetical equally weighted aggregate portfolio and found concentrations across industry, geography and sponsor relationships. So shocks are correlated as in COVID-2020 Q1.

- BDCs hedge these shocks with bank lines & cash isn’t the backstop. Liquidity insurance from banks is. Which means that banks didn’t get dis-intermediated, they moved upstream!

- Banks survived the 2023 regional bank crisis and kept funding BDCs. You’d expect bank stress to reduce BDC liquidity. Nope.

- Shared liquidity creates a tragedy of the commons. Lets say several firms share one BDC’s liquidity pool. So each firm thinks that if they need $$, the BDC will pony up. And consequently spend very little effort managing their own liquidity. So liquidity insurance itself makes firms less prudent and introduces moral hazard!

- BDCs intentionally ration liquidity. The BDCs reserve only about 53¢ to each $1 of commitment, basically choosing not to buy enough insurance against the worst possible scenario. Not surprisingly they optimize for themselves, not society.

David Krause [4] answers the question whether tokenization changes any of this? Using Maple Finance’s syrupUSDC and SYRUP tokens as case studies, his answer is no. Tokenization improves transparency. It changes the wrapper, not the economics. Default risk, liquidity mismatch, leverage, sector concentration. They all travel with the asset, whatever rails it rides on.

The sky is falling! For real tho?

Before this wave of papers landed, I took a run at this exact question myself, a couple of months ago. Different study, by Jang, Kim, and Sufi at UChicago. They built a dataset matching the near-universe of US businesses to UCC filings, BDC data, PitchBook, and a Google Vertex AI classification of PE ownership. Two numbers reframed the whole thing for me:

- Direct lending touches only about 2.5% of US middle-market firms. Banks and finance companies are around 60%.

- Roughly 75% of direct lending borrowers are PE-owned.

So direct lending isn’t a broadly distributed credit channel. It’s a PE financing arm. It clusters in a few industries and a handful of cities, and its path to the rest of the economy is narrow. Where PE doesn’t exist, direct lending is basically absent. That doesn’t make the risk small. It makes it sectoral and concentrated, not systemic. Which, as it turns out, is exactly where this new batch of papers keeps landing.

(I broke that paper down in a LinkedIn post a couple of months ago, including the due-diligence questions allocators should be asking their direct lending managers. You can read it here: https://www.linkedin.com/posts/activity-7445564969900855298-Kb2f )

Leonard U. [5] asks

“Is Private Credit the next 2008?”

He comes away with a completely unsatisfying answer. It’s obviously not a systemic catastrophe but not completely benign either. His view is that most private credit losses are likely to stay inside funds and their investors because today’s system has:

- More regulation

- Less leverage than pre-2008

- Sophisticated institutional LPs

- Locked-up capital structures

Unlike 2008, depositors and taxpayers are not directly exposed. He walks through 4 transmission mechanisms that could carry stress through the market.

- Back leverage into banks. Private Credit funds use warehouse facilities, leveraged mezz structures and fund leverage, and consequently in a downturn loan losses rise, banks tighten facilities, refi gets difficult and asset values fall, creating a feedback loop.

- Sponsor-to-sponsor exits. PE borrowers repay old loans using debt raised by the new sponsor. So when M&A slows, exit liquidity disappears, valuation multiples compress, recoveries worsen and direct lenders suffer. Whole ecosystem is a refi chain.

- Insurance companies increasingly buy private credit exposure through rated structures. These carry much less leverage than pre-2008 securitizations, but they still create another layer of system leverage.

- Multi-managers are allocating more to private credit. If they experience losses elsewhere, they may liquidate positions and transmit stress across markets through forced deleveraging.

The counter-intuitive findings :

- Biggest danger is the liquidity structure not defaults.

- Institutional private credit may be fine while wealth channel products suffer. So the same GP can have excellent institutional funds but fragile evergreen products. Identical asset quality differing only in liability structure.

Another paper by Shinya Hanamura [6] poses the question we all heard in the media:

Could a classic bank run type situation happen in Private Credit?

It’s a positive/theoretical model where he applies Diamond-Dybvig bank-run structure and Morris-Shin global games as the mathematical tools and he applies it to private credit to derive a unique run threshold.

TL;DR : You don’t need deposits to have a bank run, you need only a coordination problem. He finds:

- Run can occur without bad loans. Most people think defaults cause runs. But runs themselves causes defaults.

- Illiquidity isn’t the problem. Private credit is inherently illiquid, but it becomes dangerous only when combined with liquidity promises.

- Better transparency can worsen runs. Fascinating because I thought more info would stabilize the markets. But frequent marks and bad news can synchronize investors and everyone runs simultaneously. Apollo recently has been talking about doing this and while I approve of the spirit, the model says it will likely increase run probability.

- Gates are not evidence of failure. People interpret gates as “this fund is broken” but the model gates change the game by removing the first mover advantage (elimination of run equilibria).

- Diversification doesn’t eliminate runs. It can reduce losses but runs are about liability structure and investor expectations.

- Leverage and redemption rights interact nonlinearly. Small increases in either leverage or redemption rights suddenly push the system past a tipping point and a seemingly safe structure can abruptly become unstable. This is in line with my thinking as well and I posited this might resemble a Bingham plastic rheologically. Here’s my post: https://www.linkedin.com/posts/sureshnageswaran_private-credit-redemptions-behave-like-wet-share-7443452842318663681-yMdz

Stefan Hepp [7] delivers the most reassuring finding (also unsettling) by running a RoE decomposition on a representative large scale levered DL fund. He explicitly states that his work is interpretive and framework-based and not econometric.

Paraphrasing his paper:

Forget about whether Private Credit is the next 2008. The more interesting question is who survives the next cycle.

Reassuring finding: Even severe stress implies return compression as opposed to principal impairment for diversified senior-secured portfolios. What’s unsettling is that the actual fragility sits in the tail with smaller lenders, insurance-linked balance sheets and equity tranches. It points to consolidation across the $1.5T market.

- Biggest risk isn’t defaults. You would normally think Default->Losses->Collapse. But he says it’s Funding stress-> Refi issues-> Wider Spreads-> Return Compression -> Capital Migration.

- Gates indicate strength not weakness. They exist to prevent fire sales and without them perpetual vehicles (I know the jury is divided on these) can’t own illiquid loans and even BCRED eventually went back to 5% cap in Q2 2026.

- Market is sorting private credit and not repricing it. Investors aren’t fleeing the asset class, they’re discriminating among managers. Leyla Kunimoto points out the same thing in her post here as well: https://www.linkedin.com/posts/lkunimoto_this-is-a-great-chart-on-many-levels-let-share-7464319280222871552-vPIJ

- Bigger is safer. Unlike PE where concentration is viewed negatively, in private credit scale itself is diversification. Because upside is capped and downside is large, diversification matters more than finding outlier winners. So a single 200-loan platform suppresses left-tail risk better than 5 30-loan specialists.

- Beware of spread compression even more than defaults. 2023–25 vintages were originated with very thin spreads and SOFR increases kept yields looking attractive, but risk premia compressed materially. Next cycle may reveal that investors weren’t paid enough.

- Large platforms are simultaneously concentration risks and stabilizers. They act as shock absorbers because of their ability to move risk internally, support funds, and refinance.

- Secondary market discounts don’t necessarily mean NAVs are wrong. A buyer demanding 17% IRR on assets yielding 11% must buy below NAV. The discount reflects the buyer’s cost of capital, not necessarily inflated marks.

- Next cycle will resemble the post-2000 Hedge Fund industry with smaller firms disappearing, assets concentration, bigs get bigger, improved diversification and stress producing consolidation and not systemic collapse.

Now let’s look at Joseph Hurd [8] on the demand side. Also not econometric and more a conceptual mechanism analysis relying on Minsky fragility, Stiglitz-Weiss etc.

Private credit can help keep companies alive by extending maturities, amending terms, capitalizing interest, or avoiding public default recognition. That can be stabilizing. But it can also mask whether the borrower’s actual business volume and cash flow are deteriorating.

So for private credit, Hurd’s lens would say:

Do not only ask whether the loan is current. Ask whether the borrower’s transaction volume still clears at the price and financing terms required to support the debt.

This is especially relevant for borrowers exposed to:

- consumer affordability,

- auto sales,

- housing turnover,

- equipment purchases,

- inventory financing,

- distribution networks,

- high fixed operating costs.

Rising prices can be sustained for a long time when credit expansion, longer maturities, and looser payment assumptions keep converting strained buyers into closed transactions. But that doesn’t remove the affordability ceiling. It just defers it.

And once borrowing limits or risk thresholds finally bind, adjustment moves from prices to quantities and volume dries up. That’s a useful reminder because a market can look fine on price right up until it stops clearing at all.

The lag problem

The quietly important one in the paper stack for me was Hoyeon Kang, FRM [9] who compares the CLOIE (JPMorgan CLO index discount margins, BB/BBB tranches that MTM through dealer quotes) and the CDLI (Cliffwater DL Index). On a sidenote, Blake Nesbit does a quarterly rundown of the CDLI on youtube, totally cracked, love it.

Core claim is:

CLO market spreads move first and CDLI lags by one quarter.

Geltner unsmoothing shows reported quarterly volatility is understated by 26%. Max drawdown deepens from -6.7% to -9% once you unsmooth. He also uses the Lincoln Senior Debt Index as an external validation benchmark and BDC price-to-NAV discounts as a public equity market signal.

- CDLI is lagged. I suspect the other benchmarks are too (Stepstone Kroll, MSCI NA DL Index). Anyone want to write a paper on this with me?

- Market knows before the benchmark knows. Which is why CLO spreads and BDC stocks react before CDLI. In 2022, CLOIE BB discount margins widened sharply while CDLI continued reporting positive returns and only modest declines.

- Lag is concentrated in appreciation returns and not income returns. So CDLI total return = Income return + Valuation return. And Kang finds that CLOIE BB margins lead the appreciation component of CDLI by one quarter, but do not significantly predict income returns. That makes sense, the income stream is stable but fair-value adjustments are where the market stress should show up.

- Unsmoothing shows 1.35x greater volatility, worser drawdown and Sharpe ratio falling materially. Shocking (not).

- As an allocator you may want to monitor CLO BB/BBB spreads, BDC price-to-NAV, LL spreads and secondary market discounts as early warning indicators.

Where the system actually connects

If you want to know how a Private Credit problem becomes a banking problem, three papers map the wiring with a fourth building the frame.

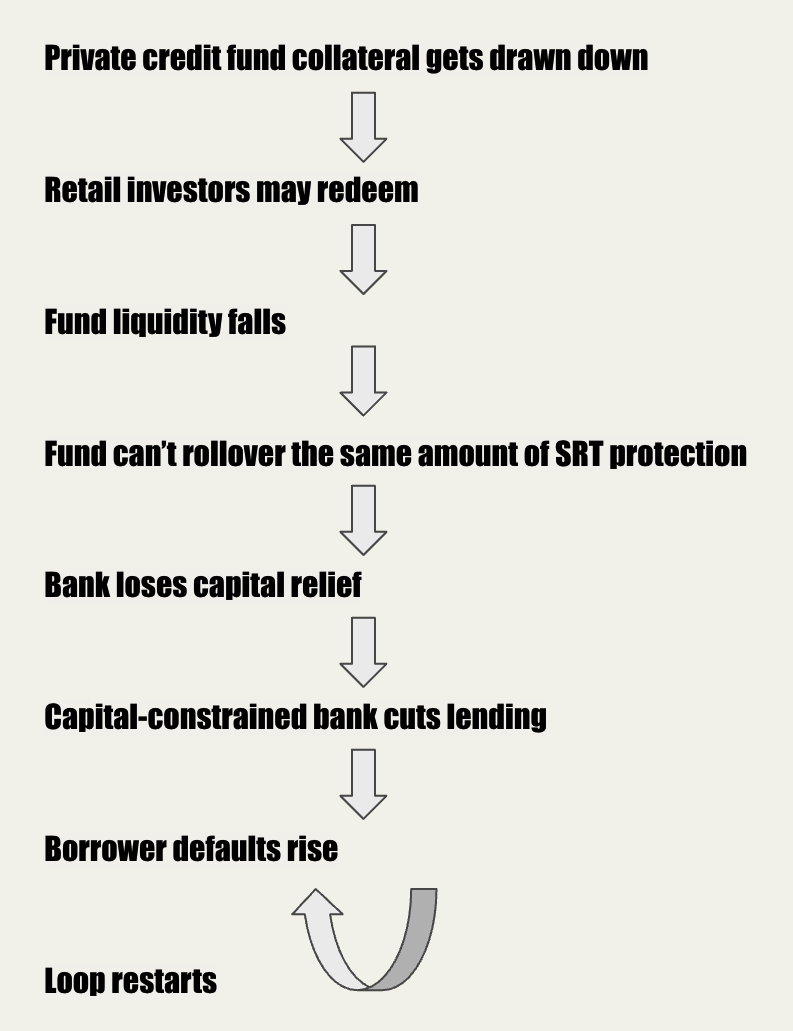

Riccardo Russo [10] from Bocconi’s BAFFI centre, models a contagion loop running through the SRT (Synthetic risk transfer) market. Private Credit funds have quietly become big sellers of protection to banks there. The loop switches on through two features the literature has barely formalized together:

- The circular leverage baked into SRT financing.

- The liquidity mismatch from semi-liquid funds sitting on the other side of the trade.

Put them together and you can get a “protection gap.” That’s a quiet erosion of the capital relief the banks thought they’d bought.

Ly Nguyen [11] at Rice, asks:

Is Private Credit replacing banks or becoming part of the banking system?

She uses the Small Business Credit Availability Act of 2018 as a quasi-natural experiment. The SBCAA reduced BDC asset-coverage requirements from 200% to 150%, effectively allowing BDC leverage to rise from about 1:1 D/E to 2:1 D/E. It also relaxed disclosure and communication requirements for publicly traded BDCs. Nguyen treats this as an exogenous expansion in private-credit supply.

- Small banks get more aggressive & compete downstream. They defend their middle-market turf by lowering rates, loosening underwriting, expanding lending volume and pushing into new geographies.

- Large banks do the opposite and move upstream to become wholesalers. They retreat from direct lending and fund the Private Credit funds instead, picking up favorable risk-weight treatment along the way. I was curious as to why large banks prefer lending to Private Credit funds instead of lending directly to firms (just cut the middleman, no?). Turns out thats because loans to PC intermediaries are senior/secured and get more favorable regulatory capital treatment, also monitoring cost is lower.

- The punchline is the selection problem. The banks with the weakest balance sheets have the strongest incentive to run that arbitrage. That’s exactly the wrong group to be leaning in.

Kenneth Ford and Akhtar Siddique [12] posit that:

Institutional capital is stabilizing in normal times, but can amplify stress when its own funding channel becomes constrained.

They put hard numbers on the transmission. A 100 bps rise in CLO AAA spreads passes through to a 100 - 140 bps rise in securitizable institutional loan pricing. The same borrower can face different loan pricing depending on whose capital is behind the loan.

Bank balance sheet capital ≠ CLO-funded Institutional Capital ≠ PC Committed Capital

Bank-dependent loans? No measurable effect. And the sensitivity is stronger when undeployed capital is high. So the dry powder everyone treats as a shock absorber might, under the right conditions, amplify the shock instead!

Few takeaways:

- More Institutional capital can mean more fragility. In normal times institutional capital means market depth. In stress, institutional capital equals a common funding constraint.

- Dry powder isn’t $$ sitting in a checking account. It’s contingent capital to be deployed only if funding, investor appetite, collateral terms, market clearing conditions still work.

- Credit stress doesn’t hit all loans equally (it matters who the lender is).

- Pricing and allocation adjust on different margins. Exposed securitizable loans reprice wider and small marginal deals get withdrawn. In other words, the market has both a price channel and a quality channel.

When liquidity stress rises, the market adjusts in two ways:

- Large/institutional/CLO eligible deals -> price goes up

- Smaller/marginal deals -> deal may not even clear

Giancarlo Mazzoni [13], at the Banca d’Italia is next. BTW, what is up with Italians and finance papers on SSRN, something in the waters of the Tiber?

He zooms out the furthest. He extends Merton’s contingent-claims logic into one structural architecture. It can hold banks, insurers, funds, and Private Credit vehicles in a single frame, all connected through common assets and runnable liabilities. It’s the skeleton the others put flesh on. It’s a formal supervisory framework, not an empirical paper.

Mazzoni gives supervisors a Merton-style structural toolkit for the post-bank financial system, where the relevant question is no longer just “will the bank default?” but “where has the risk moved, what form has it taken, and through which channel can it return?”.

The governance premium

Under all the macro plumbing sits a more durable question.

What separates the funds that survive a cycle from ones that don’t?

Three papers land on the same answer. Nope, not yield.

Chung Hei Sing [14] argues that performance dispersion in Private Credit comes far less from entry yield or strategy labels than from governance capability. That means covenant design, information rights, monitoring intensity, and the ability to step in when a borrower wobbles. His phrase for the asset class is: “control without ownership.” It sits right between public credit, which relies on market exit, and private equity, which relies on owning the thing.

John Christiansen’s MUNRO framework [15] reads like a direct answer to the due-diligence failures the recent litigation exposed at First Brands and Tricolor.

Private credit origination should not be treated as a deal-level judgment call. It should be treated as a portfolio-level decision under uncertainty.

Instead of hardening the same old checklist, he reframes the origination decision itself. It becomes a stochastic, multi-objective, distributionally robust portfolio problem. Covenant pricing, the Bayesian value of information, and real-options thinking all get pointed at one question. Whether to lend, and on what terms.

Normally deal teams are asking if they like this particular borrower, or is the spread high enough or the covenants acceptance and can you get comfortable after diligence.

MUNRO framework

- A loan backed by a top-quartile sponsor and a loan backed by a weak sponsor should not have the same tail-loss model, even if the headline leverage looks similar.

- Don’t use flat illiquidity premiums, rely on the fund’s own liability structure. A closed-end institutional fund and a semi-liquid BDC should not price illiquidity the same way.

- Covenants as real priced options. I almost picked up the phone to call Elham Saeidinezhad, Ph.D. and Uri Ravid, this is exactly their thesis. Read my post on their work here: https://www.linkedin.com/posts/sureshnageswaran_in-private-credit-secondaries-credit-risk-share-7407092734123200512-8hGh

- Bayesian value-of-diligence pricing. For every open diligence item, the framework estimates Expected reduction in uncertainty vs cost of doing the diligence. The output is a ranked list of diligence questions with a dollar value of information.

- Pareto-frontier commercial terms optimization. It produces a Pareto frontier of acceptable term sheets. A term sheet is “non-dominated” if no other package is better on all relevant dimensions. How cool is that? He applies the efficient frontier concept here. So your Investment Com doesn’t get Approve/Reject. You give them the feasible tradeoffs and ask them to choose the package that matches the fund’s current portfolio objectives.

- Wasserstein-ball distributionally robust optimization layer. In simpler terms, instead of optimizing for the loss distribution you think is true, optimize for the worst plausible loss distribution near your observed data.

Baraa Shaheen’s legal theory/bankruptcy governance essay on fiduciary inversion [16] states that under bankruptcy law the people who exercise the most control over a restructuring often bear the least formal fiduciary responsibility for it.

That control runs through DIP financing structures, advisory relationships, and pre-negotiated deals. So the investors left holding residual risk across the capital structure are frequently the ones with the least visibility into how value actually gets carved up.

Case in point is Revlon where the confirmed plan gave 82% of reorganized equity to BrandCo B-2 lenders and 18% to 2016 term loan lenders, with unsecured creditors getting warrants or a share in the residual $44M settlement pool.

How we got here

For the longer arc, Claudia Zeisberger and her INSEAD colleagues [17] trace LBO debt structuring across three eras:

- The classic multi-tranche bank-syndicated model before 2008.

- Following ZIRP decade

- Private-Credit-dominated landscape of 2026.

Together they made the unitranche and the cov-lite package the default instruments of modern leveraged finance. The covenant erosion they document, from full quarterly maintenance packages down to cov-lite, is exactly the inheritance this cycle is now stress-testing.

The instruments changed, lender base changed, and covenant package changed. But the basic math of leverage did not change.

3 things still matter: seniority determines cost, coverage ratios constrain debt capacity and leverage magnifies both gains and losses.

So what now?

Daniel S. Lim [18] goes straight at the structural failure behind the cascade.

The redemption problem is not mainly a disclosure problem or a manager-discretion problem. It is a legal-architecture problem.

His proposal is a functional separation:

- A productive asset pool on one side.

- A separately capitalized redemption-liquidity pool on the other.

- Replenishment governed by pre-committed mechanical rules.

- Redemption capacity set by objective liquidity tiers, not discretionary gates.

- Valuation safeguards by independent valuation checks & NAV adjustment triggers

It treats liquidity as an enforceable structure, not a policy the manager reaches for under duress. Which is precisely the thing Q1 exposed. So smart contract maybe?

Past reform, three papers sketch the frontier:

- Shashi Tiwari [19] argues tokenized securities stay peripheral until the market solves institutional finality, not technology. You need an authoritative record, the function CSDs provide today. A shared ledger on its own doesn’t replicate it.

- Yueru Li [20] proposes cash-flow shorting. It’s a market design that lets people trade negative expectations on private, illiquid cash flows through collateralized claims on verified realized cash flows. In plain terms, it would give the asset class the price discovery it conspicuously lacks.

- Robert Zimmerman [21] comes at it from a completely different angle. He models a nine-step contagion running from a single distressed AI data-center project up through surety, lending, SPV, securitization, and Private Credit layers. It’s a good reminder. The next stress might arrive from the asset side, not the liability side, as the $700 billion-a-year hyperscaler buildout pulls Private Credit into construction-execution risk it has never really priced.

And the backdrop frames all of it. The August 2025 Executive Order opened 401(k) plans to alternative assets. So the retail base that just got tested is about to get a lot bigger. Whatever resilience Q1 showed is about to be asked to scale.

Final thoughts

What I’m thinking after reading all of it is that the research doesn’t support the panic. It doesn’t support the complacency either. More like an uncomfortable third position.

The architecture held this time. But look at why. Sponsors happened to have capital and the will to deploy it. Prospectuses happened to carry discretion and the law happened to allow pro-ration. None of those is guaranteed in a bigger or more correlated shock.

The reform agenda these papers point to is useful:

- Lim’s liquidity separation

- Kang’s faster valuation signals

- Real transparency into the bank-and-fund nexus that Russo, Nguyen, and Ford mapped out.

For those of us building the analytical infra for this market, the exposure indices, the covenant-liquidity measures, the orchestration layers between the data and the decision, this is the moment those tools stop being academic.

Question for you. Which of these findings actually changes how you’d underwrite or allocate today?

This was fun, hope you enjoyed it. LMK.

P.S. Didn’t use AI to do any of this, just to let my 11-yo know that authenticity matters.

References

The bracketed numbers in the text map to this list. All papers are on SSRN.

- Retalization of Private Credit Revisited: Three Private Substitutes for the Public Backstop in the Q1 2026 BDC Cascade. Luka Stanisljevic, May 2026. https://ssrn.com/abstract=6740281

- The Funding Structure of Direct Lenders. Elisavet Mistopoulou and Sascha Steffen, June 2026. https://ssrn.com/abstract=6853858

- Credit Commitments by Nonbanks. Jing Huang and David X. Xu (Texas A&M and SMU), May 2026. https://ssrn.com/abstract=6843664

- Same Risk, New Wrapper: Contagion Between Traditional and Tokenized Private Credit. David Krause (Marquette University), 2026. https://ssrn.com/abstract=6409678

- Private Credit: A Slow-Motion Train Wreck, or Much Ado About Nothing? Len Umantz, April 2026. https://ssrn.com/abstract=6686398

- Structural Vulnerability and Mathematical Analysis of Bank Runs in the Private Credit Market. Shinya Hanamura, May 2026. https://ssrn.com/abstract=6724598

- The Plumbing Beneath Private Credit: Structure, Stress, and the Coming Consolidation of a $1.5 Trillion Market. Stefan Hepp (University of Chicago Booth), June 2026. https://ssrn.com/abstract=6918820

- When Credit Stops Clearing Markets: Affordability Ceilings and Volume Driven Systemic Stress. Joseph E. Hurd, May 2026. https://ssrn.com/abstract=6730658

- Appraisal Lag and Market Signals in Private Credit: Evidence from CDLI and CLO Index Spreads. Hoyeon (Joe) Kang, June 2026. https://ssrn.com/abstract=6916998

- Private Credit, SRTs and the Banking System: Mind the Protection Gap. Riccardo Russo (Bocconi University, Baffi CAREFIN), May 2026. https://ssrn.com/abstract=6897519

- Are Banks and Private Credit Complements or Substitutes? Ly Nguyen (Rice University), May 2026. https://ssrn.com/abstract=6714179

- Whose Capital Is It? Liquidity, Institutional Funding, and Credit Market Outcomes. Kenneth Ford and Akhtar Siddique, May 2026. https://ssrn.com/abstract=6847420

- A Structural Model for Banks and NBFIs. Giancarlo Mazzoni (Banca d’Italia), May 2026. https://ssrn.com/abstract=6747398

- Private Credit as a Structural Allocation: Why Governance, Not Yield, Determines Long-Term Outcomes. Chung Hei Sing, 2023. https://ssrn.com/abstract=6622838

- MUNRO: A Multi-Objective, Distributionally Robust Decision Framework for Private Credit Origination. John Christiansen (University of Edinburgh), April 2026. https://ssrn.com/abstract=6674438

- Fiduciary Inversion in Bankruptcy: Influence, Priority, and the Limits of Doctrine. Baraa Shaheen, April 2026. https://ssrn.com/abstract=6683498

- LBO Debt Package Structuring: From Classic Syndicated Structures to the Age of Private Credit. Claudia Zeisberger, Ugne Kupryte, Muhammed Al Yakub and Nicolas Metzger (INSEAD), 2026. https://ssrn.com/abstract=6812722

- Study on Redemption Mechanisms in Private Equity and Credit Funds Investing in Illiquid Assets. Daniel S. Lim (DSML Holdings), 2026. https://ssrn.com/abstract=6823540

- From Ledger Control to Institutional Finality: Why Tokenised Securities Need Authoritative Market Records. Shashi Tiwari, March 2026. https://ssrn.com/abstract=6783278

- Shorting Without Borrowing: Markets for Negative Cash-Flow Expectations. Yueru Li, May 2026. https://ssrn.com/abstract=6850881

- Disrupting Delivery: Why America’s AI Infrastructure Build Will Fall Short. Robert Zimmerman, May 2026. https://ssrn.com/abstract=6843218