Machine Learning in Alternative Investments: From Due Diligence to Continuous Re-Underwriting

Most allocator analytics stacks are optimized for point-in-time due diligence, not continuous conviction management. Mapping the production ML stack to allocator reality.

Institutional allocators spend time defending, monitoring and re-validating decisions already made. However, most alternative investment analytics stacks are optimized for point-in-time Due Diligence and not for continuous conviction management.

This is a gap. It matters most under regime change.

Across private equity, private credit, real assets, and hedge funds, more than 70% of allocator effort is consumed by:

- Ongoing monitoring

- Exception analysis

- Re-underwriting under changing market conditions

The tools used to underwrite an investment are often not the tools used to monitor it and almost never the tools used to re-underwrite it when assumptions break.

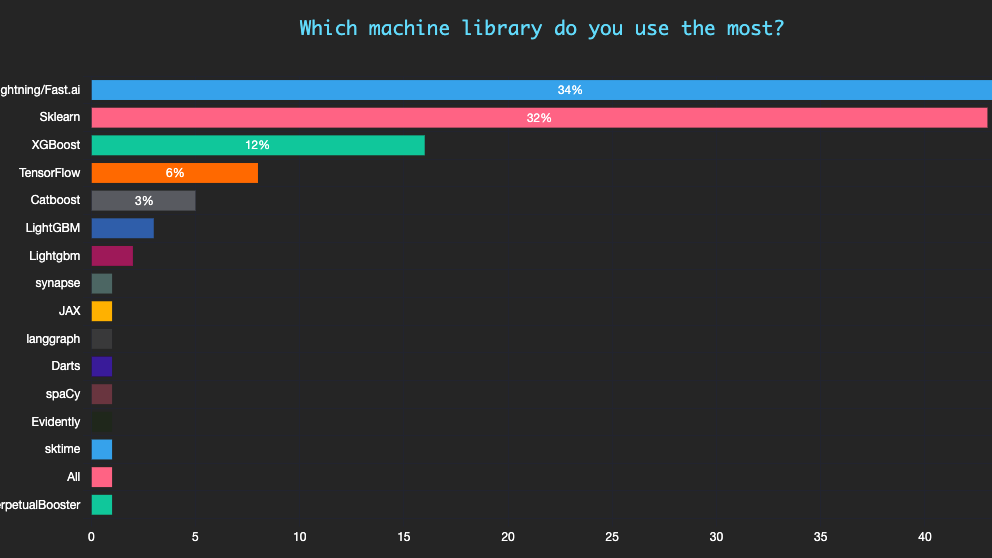

The State of ML in Production (2025) report from the Institute for Ethical AI & Machine Learning offers a useful signal of how leading institutions across industries are addressing this problem in practice. When mapped to allocator workflows, a clear pattern emerges.

Takeaways for Investment Committees

Where does machine learning sit in the investment process?

Three observations:

1️⃣ Delayed recognition of changed assumptions is the primary driver of loss in illiquid Alts (not poor underwriting as commonly believed).

2️⃣ Monitoring and re-underwriting workflows DO NOT share architecture with Diligence workflows, creating blind spots exactly when risk is shifting.

3️⃣ Continuous Re-Scoring, Drift Detection and Governance is where Machine Learning stacks are converging. One-off insight isn’t as valuable.

Machine Learning Mapping to Allocator Reality

1️⃣ The Tabular Data Workhorses 🐎

XGBoost · LightGBM · CatBoost

These gradient-boosting frameworks dominate wherever alternative investing actually lives:

- Sparse, noisy, tabular data

- Mixed numeric and categorical features

Bang-for-Buck Use Cases

- Default and Impairment predictions in Private Credit portfolios

- Secondary Pricing for illiquid PE stakes

- LP commitment pacing and liquidity forecasting

- DPI and Cashflow sensitivity analysis

Why This Matters

These models enable re-scoring (as opposed to storytelling). They surface early signal deterioration well before it appears in NAV marks or quarterly reports.

2️⃣ The Interpretable Core ⚽

Scikit-learn

Despite the rise of deep learning, classical “boring” ML remains central to allocator analytics.

This powers:

- Credit risk scoring for direct lending portfolios

- Factor-based return attribution in hedge fund strategies

- Comparable Clustering for private company valuation

- Principal Component Analysis (PCA) for dimensionality reduction in multi-asset portfolio construction

Why This Matters

Interpretability is not a “nice-to-have” in alts. It is a hygiene factor for LP communication, IC defensibility and model risk governance.

3️⃣ Unstructured Data Engines 💡

PyTorch · Lightning · Fast.ai · spaCy

These frameworks translate qualitative risk into analyzable signals.

They support:

- NLP-driven parsing of credit agreements, PPMs, LPA, side letters, etc.

- Detection of covenant amendments and documentation drift

- Analysis of management discussion text in private company financials

- Computer vision for real estate valuation using imagery

- Alt data analysis in PE Diligence (e.g., satellite or transaction data)

Why This Matters

This is how “qualitative diligence” becomes monitor-able and repeatable, not episodic/manual.

4️⃣ High Performance and Advanced Modeling 🏃

TensorFlow · JAX

These libraries are used where scale, speed or mathematical flexibility is required:

- Large-scale time-series modeling in commodities and infrastructure

- Non-linear portfolio optimization across multi-strategy funds

- Bayesian inference for illiquid asset volatility estimation

- Monte Carlo simulations for long-duration real asset projects

Why This Matters

Provides stress-aware modeling when linear assumptions break—i.e., exactly when allocators most need analytical clarity.

5️⃣ The Missing Layer in Allocator Stacks 🔑

Evidently

Model drift, Data drift and Regime change are inevitable.

Allocator platforms need to detect them explicitly and proactively:

- Monitor stability of credit and valuation models as conditions shift

- Detect regime changes in return patterns

- Validate that private market models remain reliable over time

- Support model risk management and governance requirements

Why This Matters

Undetected drift does not cause immediate loss. It’s worse (more damaging) because it causes late recognition.

The Signal Behind the Tooling

The dominance of PyTorch and Scikit-Learn reflects a dual reality in Alternatives:

- The need for sophisticated modeling of unstructured and complex data

- The requirement for interpretable and defensible models

The strong showing of gradient boosting methods (XGBoost, LightGBM, CatBoost) reflects the structured and tabular nature of private markets. The need is to re-score risk continuously and not just ex post.

Key Takeaways for CIOs and Investment Committees 🎯

This isn’t about which Machine Learning library is most popular.

Modern alternative investment analysis is shifting from static evaluation to continuous re-underwriting.

Current State: Most allocator technology stacks remain optimized for:

- Initial due diligence

- Periodic reporting

- Backward-looking performance attribution

Required State: NOT optimized to:

- Detect model and assumption drift

- Re-score risk as market regimes change, or

- Re-underwrite exposures before impairment becomes visible in NAV

The Pattern

ML libraries showing up most consistently in production are not experimental tools. They reflect a deliberate architectural shift toward:

- Interpretable models that can be defended to LPs and regulators

- High-performance tabular analytics for illiquid assets

- Continuous monitoring of model stability and data integrity

For CIOs: The Decision

The decision is no longer whether to use machine learning, but where it sits in the investment process.

→ Embed ML into ongoing monitoring and re-underwriting workflows to gain earlier signals, faster response times, and tighter governance.

→ Don’t treat ML as a diligence-only capability.

→ The idea is to discover risk BEFORE it surfaces in valuation marks, ex ante.

That’s the edge.

Resource

My colleague Ilya Katsov at Grid Dynamics has written an entire book on Enterprise AI. Download it here: https://www.enterprise-ai-book.com/